Smart money management with guide to essential financial terms like leverage, liquidity, volatility, net worth, credit score, SIP, emergency fund, asset allocation, arbitrage, index, treasury yield, revenue vs profit, capex vs opex, ROI, and ROE kept exactly as provided and enhanced with practical insights for Indian investors.

Table of Contents

ToggleWhy these terms matter?

If you want smart money management to become second nature, understanding core financial terms is non-negotiable. These concepts shape daily financial choices from loans and investments to emergency planning and long-term wealth building. Below is your original content, kept intact, followed by practical takeaways that connect each idea to smart money management.

Essential Financial Terms You Need to Know for Smarter Money Management

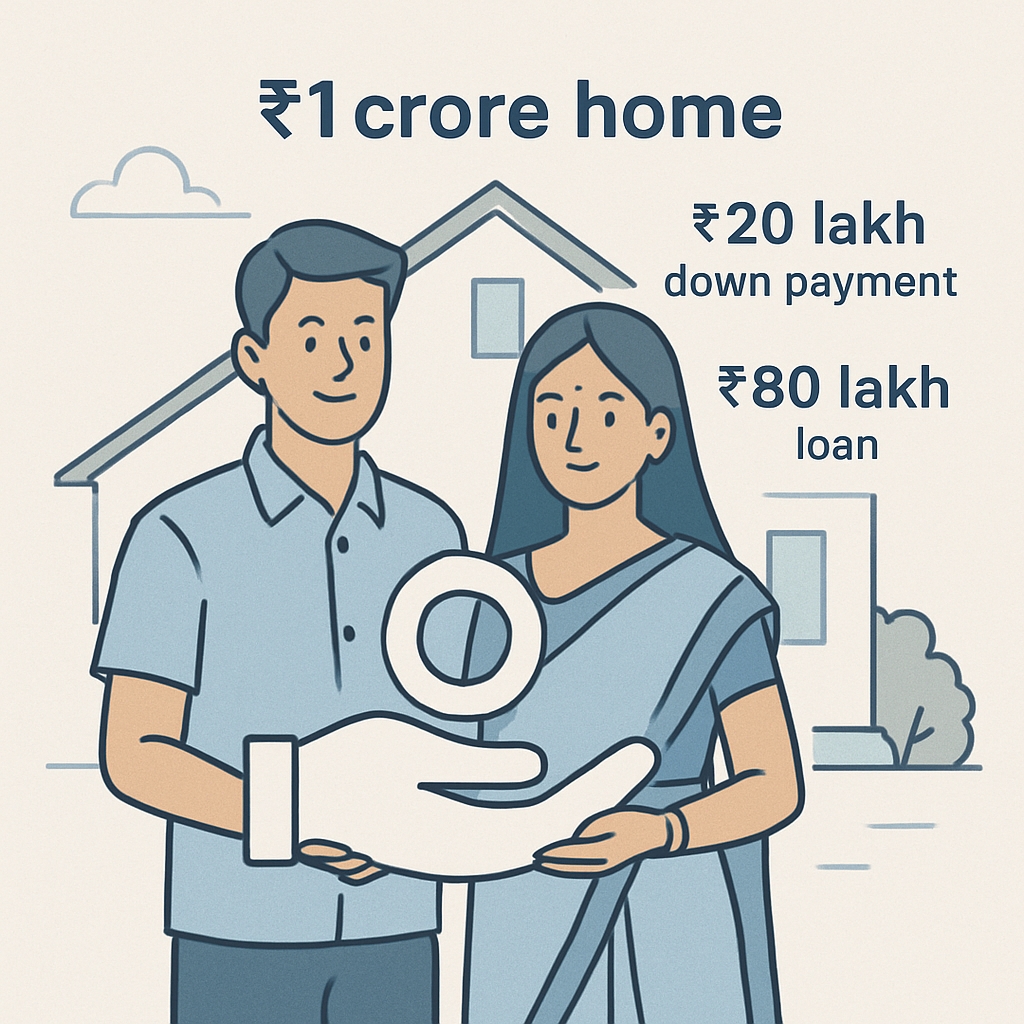

1. Leverage

What it means: Using borrowed money to increase your investment size or returns.

Example: Buying a ₹1 Cr house with only ₹20L of your own money and ₹80L loan = leverage.

Note: Leverage can multiply gains, but also losses. Handle with care.

2. Liquidity

Liquidity means how easily an asset can be turned into cash.

– Stocks are liquid — you can sell them instantly.

– Property is illiquid — selling it takes time and effort.

High liquidity means you can access your money when needed, especially in emergencies.

3. Volatility

This term describes how much the price of a security fluctuates over time.

High volatility = high risk.

A stock that moves 10% up or down daily is far more volatile (and riskier) than one that moves 1%.

4. Net Worth

Your net worth is the total wealth after subtracting liabilities from assets.

It reflects your actual financial strength, not just income.

Positive net worth = you own more than you owe.

5. Credit Score

It’s a 3-digit number that shows how trustworthy you are with credit.

Lenders like banks use it to decide your loan approvals, limits, and interest rates.

Paying bills on time and keeping credit usage low keeps it healthy.

6. SIP (Systematic Investment Plan)

SIP is a way to invest a fixed amount regularly into a mutual fund.

It builds financial discipline and helps average out market ups and downs.

Perfect for long-term goals like retirement or buying a house.

7. Emergency Fund

Money kept aside for sudden expenses — job loss, hospital bills, etc. Ideally, 3–6 months of your monthly expenses.

An emergency fund should be liquid, like in a savings account or an FD.

8. Asset Allocation

Asset allocation is how you divide your investments across different asset classes, like stocks, bonds, gold, and cash.

The goal is to balance risk and return based on your age, goals, and risk appetite.

For example, a young investor might go 80% stocks, while a retiree may prefer more bonds.

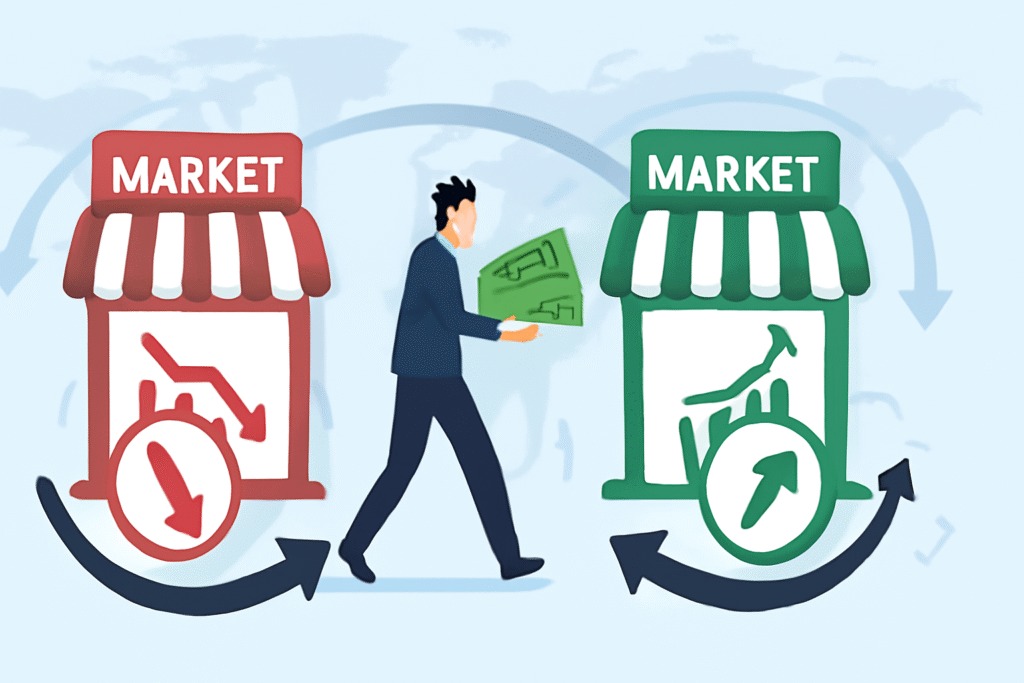

9. Arbitrage

Arbitrage is when you buy something at a lower price in one market and sell it at a higher price in another.

In finance, this could mean buying a stock on one exchange and selling it on another, where the price is slightly higher.

It’s commonly used in currency, commodities, and arbitrage mutual funds.

10. Index

An index is a group of selected stocks that represents a portion of the market.

For example, Nifty 50 tracks the top 50 companies on the NSE — it reflects how the Indian stock market is doing.

When the index goes up, it means the overall market (or sector) is performing well.

Investors use indexes as benchmarks or invest in them via index funds and ETFs.

Treasury Yield

The effective annual interest rate the U.S. government pays on its debt obligations.

It serves as a benchmark for other interest rates in the economy.

Revenue vs Profit

Revenue is the total amount of money a company makes from its sales.

For Example:

If a company sells 100 units of a product at ₹10 each,

Revenue = 100 Units × ₹10 = ₹1000

Profit is the money a company keeps after subtracting all its expenses from its revenue.

For Example:

Using the same company, if the total expenses are ₹700:

Profit = Revenue − Total Expenses = ₹1000 − ₹700 = ₹300

Capex or capital expenditure vs Opex or operating expenditure

Capex refers to the money a company spends on acquiring, upgrading, or maintaining physical assets.

For example: Buying new machinery, constructing a new building, upgrading technology infrastructure.

Opex refers to the money a company spends on its day to day operations to keep the business running.

For example: salaries, rent utilities,office supplies,maintenance cost .

ROI (return on investment)

ROI measures how much profit a company makes from an investment compared to the cost of that investment

For example:

If a company invests ₹10000 in a project and earns ₹12000

ROI = (Net profit / cost of investment) = ₹2000 / ₹10000 = 20%

ROE( return on equity)

It measures how much profit a company generates with the money shareholders have invested.

For example: if a company has ₹200000 in total equity and it earns ₹20000 in profit

ROE= (Net income / Shareholder equity) = ₹20000 / ₹200000 = 10%

Practical insights for Indian investors

To turn these definitions into smart money management, align each term with an action you can take today.

Leverage: In India, home loans can be powerful leverage if EMIs stay below 30–35% of take-home pay. Use leverage only when cash flows are stable and the asset appreciates faster than the loan rate.

Liquidity: Maintain a tiered cash system—UPI-enabled savings for instant needs, a sweep-in FD for short-term goals, and liquid mutual funds for slightly higher yields while staying accessible. This protects smart money management during emergencies.

Volatility: For long-term equity wealth, volatility is normal. Use SIPs to average costs and avoid timing the market. Keep speculative trades under a small, fixed percentage of your portfolio.

Net worth: Track quarterly. Increase assets that grow (equities, bonds, skills) and reduce liabilities with high interest (credit cards, personal loans). This is the backbone of smart money management.

Credit score: Automate bill payments, keep credit utilization under 30%, and avoid frequent loan inquiries. A strong score lowers interest costs—boosting smart money management outcomes.

SIP: Link SIPs to goals (education, retirement, home down payment). Increase SIPs annually with income hikes to accelerate compounding and smart money management.

Emergency fund: Park 3–6 months of expenses in high-liquidity options. Households with variable income (freelancers, entrepreneurs) should aim for 6–9 months to safeguard smart money management.

Asset allocation: Use a simple rule of thumb as a start, then personalize. Example: equity proportion near 100 − age, adjusted for risk appetite. Rebalance annually to maintain smart money management discipline.

Arbitrage: For most retail investors, arbitrage mutual funds can be a tax-efficient parking spot for short-term money. True multi-venue arbitrage requires speed, costs control, and strict risk limits.

Index: Broad-market index funds and ETFs can anchor your equity allocation with low costs and high diversification—key for smart money management over decades.

Treasury yield: Even though this references U.S. debt, it influences global risk appetite and can ripple into Indian bond yields and equity valuations. Keep an eye on it when making allocation shifts.

Revenue vs profit: When evaluating stocks, focus on margin trends, not just top-line growth. Expanding profits signal operational strength that supports smart money management in equity selection.

Capex vs opex: In business or startups, balance capex for growth (plants, tech) with opex efficiency (salaries, rent, cloud costs). Track ROI and payback to protect cash flow and smart money management.

ROI and ROE: For investments and businesses, prioritize projects with sustainably high ROI and companies with consistent ROE above their cost of equity. That’s disciplined smart money management.

Learn more about setting clear financial goals in our How To Retire Early At 40

Conclusion

Smart money management starts with clarity on terms, continues with disciplined execution, and compounds through consistency. By understanding and applying concepts like leverage, liquidity, volatility, net worth, credit score, SIP, emergency fund, asset allocation, arbitrage, index, treasury yield, revenue vs profit, capex vs opex, ROI, and ROE, you transform definitions into daily decisions. Keep tracking your net worth, automate good behaviors like SIPs and bill payments, maintain adequate liquidity, and rebalance annually. With these foundations and a focus on smart money management across your goals, you’ll make calmer decisions in volatile markets, protect against emergencies, and grow wealth with confidence.